The Global Adoption of the ISSB Standards

Over the past few years, sustainability reporting has undergone a major transformation. Once a voluntary and fragmented landscape, it is now becoming a structured and globally aligned reporting system.

At the centre of this shift is the International Sustainability Standards Board (ISSB), which has issued two sustainability reporting standards IFRS S1 (general requirements for disclosure of sustainability-related financial information) and IFRS S2 (climate-related disclosures). These are rapidly emerging as the global baseline for sustainability-related financial disclosures.

Jurisdictional adoption of these ISSB Standards reflects a key reality: sustainability information is no longer separate from financial performance. It is central to how organisations measure risk, create value, and ensure long-term resilience.

This article explores why sustainability reporting matters, how the ISSB was created, how it fits within the global reporting landscape, and what global adoption means for organisations today.

Why Sustainability Reporting Matters

Sustainability reporting has evolved from voluntary disclosures into a core expectation for businesses worldwide. This shift is being driven by investors, regulators, and broader societal expectations.

Climate Risk Is Financial Risk

Climate-related risks such as extreme weather, resource scarcity, and rising sea levels are already affecting business performance. These risks can:

- Disrupt supply chains

- Damage infrastructure

- Increase operating costs

- Reduce productivity

As a result, climate risk is now widely recognised as a material financial risk. Investors expect companies to disclose how these risks impact strategy, cash flows, and long-term viability.

Sustainability reporting provides the transparency needed to assess how prepared organisations are for a changing economic and environmental landscape.

Investors Need Decision-Useful Information

Modern investors increasingly integrate environmental, social, and governance (ESG) factors into decision-making. However, traditional financial reporting is backward-looking and does not capture future risks or opportunities.

Sustainability disclosures fill this gap by providing insight into:

- Risk exposure

- Long-term resilience

- Strategic positioning

- Value creation potential

This enables investors to compare companies more effectively across industries and geographies.

Introduction to the ISSB

The ISSB was established in 2021 by the IFRS Foundation aiming to address fragmentation in global sustainability reporting. Prior to its creation, companies relied on multiple frameworks such as TCFD, SASB, and GRI, often resulting in duplication and inconsistency.

Why the ISSB Was Created

The lack of global alignment created key challenges:

- Investors could not easily compare disclosures

- Companies faced multiple reporting requirements

- Regulators lacked a consistent baseline

The ISSB was created to develop a global baseline of investor-focused sustainability disclosures.

The Mandate of the ISSB

The ISSB’s objective is to deliver globally consistent standards that provide decision-useful information to capital markets.

It focuses on:

- Financial materiality

- Global comparability

- Connectivity with financial reporting

- Consistent sustainability disclosure structures

Rather than replacing existing frameworks, the ISSB builds on them to create global alignment.

Relationship with IFRS

The ISSB operates alongside the International Accounting Standards Board (IASB) under the IFRS Foundation:

- IASB → financial reporting standards

- ISSB → sustainability disclosure standards

This structure ensures closer integration between financial and sustainability reporting.

Foundations of the ISSB Standards

The ISSB did not build its standards, IFRS S1 and S2, from scratch. Instead, it leverages widely recognised global frameworks including TCFD structures and disclosures, SASB industry based metrics and the GHG Protocol standards and calculation methodologies.

In addition to this, the ISSB has agreed to develop a Practice Statement to guide companies on reporting nature-related risks and opportunities under IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures. The guidance, informed by the Taskforce on Nature-related Financial Disclosures, will clarify how to apply existing requirements without introducing new rules, with an exposure draft expected in October 2026.

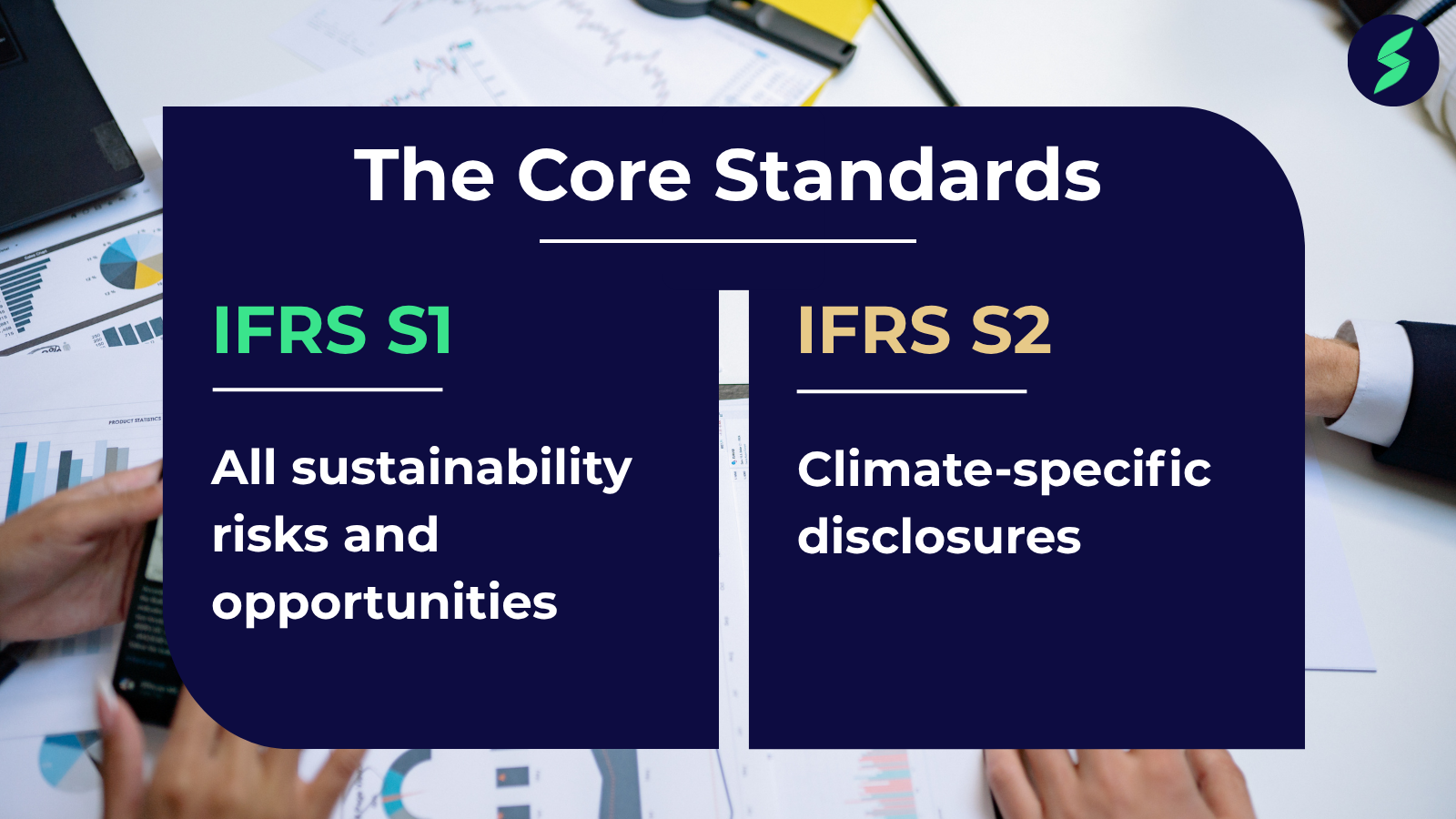

IFRS S1 and S2: The Core Standards

IFRS S1 sets out general requirements for disclosure of sustainability-related financial information, focusing on all material sustainability-related risks and opportunities that could affect enterprise value.

IFRS S2 focuses specifically on climate-related disclosures, including:

- Physical and transition risks

- Greenhouse gas emissions

- Climate scenario analysis and & resilience

- Transition planning

Both standards use the TCFD structure and require alignment with financial reporting assumptions.

Global Adoption of ISSB Standards

ISSB Standards are rapidly becoming the global baseline for sustainability reporting.

As of 2026, more than 40 jurisdictions have announced full or partial adoption or alignment with ISSB Standards.

Key Jurisdictions Moving Toward Adoption

Countries and regions include:

- United Kingdom

- Canada

- Australia

- Japan

- Singapore

- New Zealand

- Brazil and Latin America

- Nigeria

- Kenya

In addition, IOSCO has endorsed ISSB Standards and encouraged global adoption.

What Global Adoption Means

The global adoption of ISSB Standards signals a shift toward:

- A single global sustainability reporting baseline

- Greater consistency across jurisdictions

- Improved comparability for investors

- Reduced reporting fragmentation

- Stronger integration with financial reporting

This makes ISSB the emerging foundation of global ESG reporting.

Why ISSB Standards Are Becoming the Global Baseline

ISSB Standards are designed specifically for capital markets and financial materiality. This makes them highly attractive to regulators because they:

- Align with IFRS financial reporting principles

- Build on established frameworks (TCFD, SASB, GHG Protocol)

- Reduce duplication across reporting systems

- Enable scalable global implementation

As a result, ISSB Standards are increasingly becoming the core global sustainability disclosure framework.

Conclusion: The Future of Sustainability Reporting

The ISSB Standards represent a major step toward global consistency in sustainability reporting. By aligning sustainability disclosures with financial reporting, IFRS S1 and IFRS S2 provide a clear, comparable, and decision-useful framework for global capital markets.

As adoption continues to expand, organisations that understand and implement ISSB Standards will be better positioned to meet regulatory expectations, respond to investor demands, and strengthen long-term resilience.

Build Your Expertise in ISSB Reporting

To support professionals navigating this evolving landscape, the Sustainability Reporting Institute offers ISSB certification programmes designed to build practical capability in applying IFRS S1 and IFRS S2.

Find out more and enrol in our ISSB certification courses on IFRS S1 and IFRS S2.

Live Masterclass: Join us for a free masterclass on 27th May 2026 for an expert-led session on “ISSB Standards: Core Principles and Global Adoption”, exploring how different regions are implementing ISSB in practice with guest expert, Orla Carolan.

This is a free masterclass and open to all Sustainability Reporting Institute members.

Not a member? Register here for free now.