Climate Risk Disclosure: A Common Thread Across Global Reporting Frameworks

What is Climate Risk?

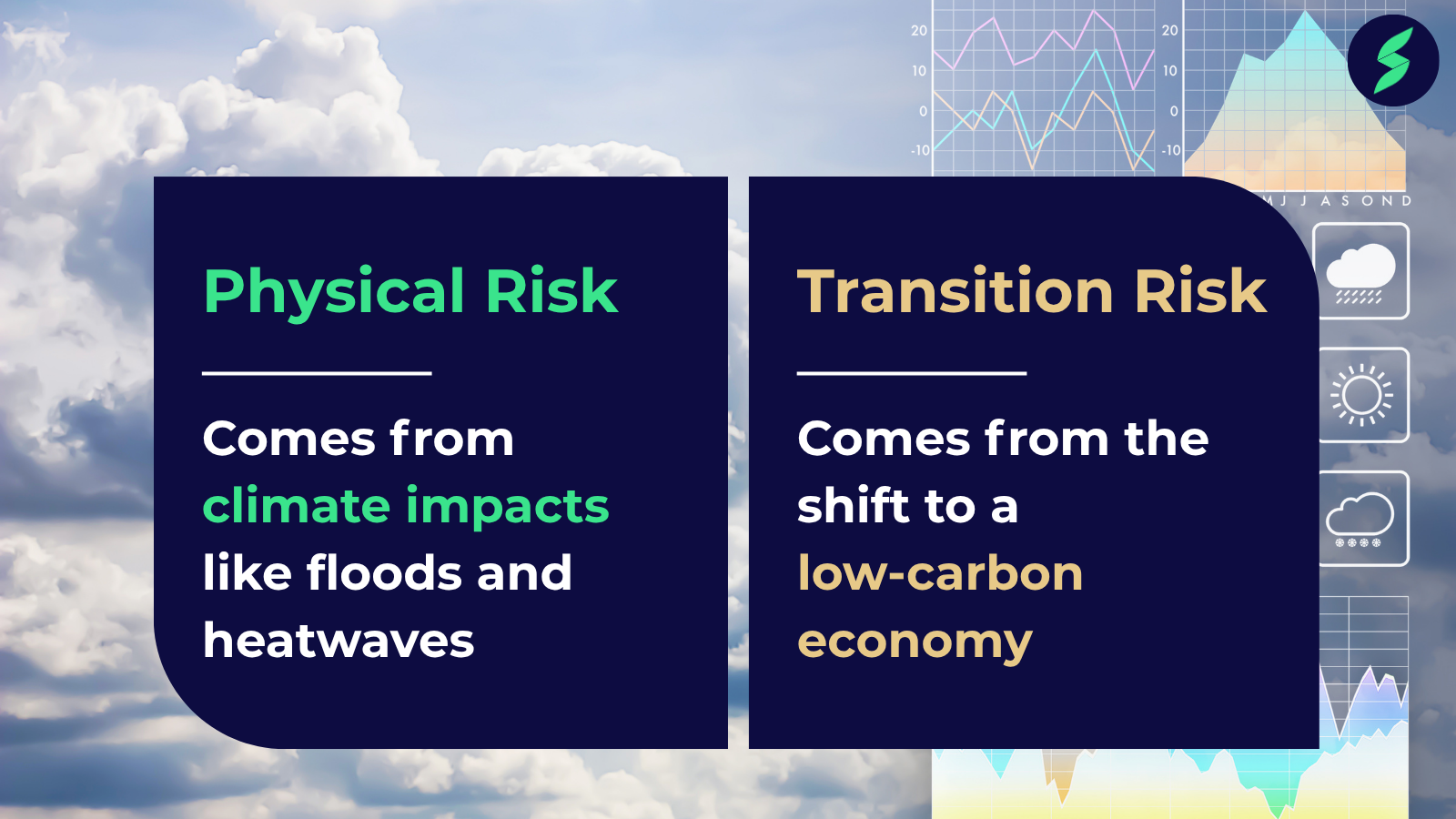

According to the TCFD framework, climate-related risks can have significant financial implications for organisations and are typically grouped into two categories; physical climate risk and transition risks related to climate.

The TCFD framework also identifies different categories of climate-related opportunities available to entities. These include opportunities for example from resource efficiencies, shifts in energy sources to renewables, new products and services or markets for example in green financing and resilience through building of climate-resilient infrastructure and diversified supply chains.

Physical climate risk explained

Physical climate risks arise from the direct impact of climate hazards on assets, operations, and value chains. They are highly location-specific and depend on where infrastructure, suppliers, and operations are located.

They fall into two categories:

Acute risks

Sudden events such as floods, storms, wildfires, and heatwaves.

Chronic risks

Long-term changes such as rising temperatures, sea level rise, and water stress.

Physical risks impact:

- Assets through damage and downtime

- Supply chains through disruption and delays

- Workforce productivity and logistics

A clear example occurred during Hurricane Helene (2024), which disrupted infrastructure in Spruce Pine, North Carolina, a critical global supplier of high-purity quartz used in semiconductor manufacturing. A single local event created global supply chain disruption.

Transition risk explained

Transition risks arise from the shift toward a low-carbon economy. They reflect how policy, technology, market behaviour, and legal pressures reshape business models.

Key drivers include:

- Regulation and policy (carbon pricing, disclosure rules)

- Technology change (low-carbon innovation disruption)

- Market shifts (demand for low-carbon products)

- Legal and reputational pressure

These affect organisations through:

- Revenue and competitiveness

- Cost structures and compliance burden

- Asset valuation and stranded assets

- Business model transformation

Unlike physical risks, transition risks evolve gradually but can significantly reshape long-term competitiveness.

What is climate risk assessment?

A climate risk assessment is the process by which a company identifies, evaluates and quantifies the potential financial impacts of climate change on its business, including both physical and transition risks and climate-related opportunities.

The primary methodological tool in completing these assessments is climate scenario analysis which is a structured process of stress-testing the business against a range of plausible future climate pathways.

It is now a core requirement under global reporting frameworks such as IFRS S2, ESRS and TCFD (which now forms the basis of disclosure requirements under IFRS S2). It is increasingly expected by investors, lenders and regulators as part of mainstream financial disclosure.

Why do extreme weather events dominate climate risk assessments?

Extreme weather events consistently rank as the most significant climate risk due to their rising frequency and economic impact.

The World Economic Forum Global Risks Report 2026 highlights extreme weather events as one of the most severe risks across short, medium, and long-term horizons, reflecting its systemic impact on global economies.

Climate risk disclosure reflected in global reporting frameworks including CSRD and IFRS S2

Climate risk disclosure is increasingly becoming mandatory across jurisdictions, with the global adoption of ISSB Standards accelerating and IFRS S2 establishing a global baseline for climate-related financial disclosures.

- CSRD (EU): Requires disclosure of material climate-related impacts, risks and opportunities under ESRS E1.

- IFRS S2 (ISSB): Requires disclosure of climate-related risks and opportunities, including governance, strategy, risk management, and metrics and targets.

- Switzerland: TCFD-aligned disclosures for large companies

- ASRS (Australia): Climate scenario analysis and transition planning

- VSME (EU): Addresses climate-related risks and opportunities, providing a simplified approach to sustainability disclosures for smaller and medium-sized enterprises.

From disclosure to decision-useful climate intelligence

The key challenge in climate risk reporting is not compliance, it is usability.

A report is only valuable if it informs decisions such as:

- Capital allocation and investment planning

- Asset resilience and adaptation strategies

- Supply chain risk management

- Scenario-based strategic planning

This requires a shift from static reporting to ongoing climate risk intelligence embedded in business processes.

Why climate risk disclosures matter

Climate risk disclosure is becoming a regulatory and financial requirement rather than an optional sustainability exercise.

Key drivers include:

- Mandatory disclosure frameworks such as CSRD, IFRS S2, SB 261, ASRS, and Swiss TCFD-aligned requirements

- Increasing investor and lender expectations

- Integration of climate risk into valuation and credit models

Beyond compliance, it supports:

- Better risk management

- Improved capital allocation

- Long-term strategic planning

- Operational resilience

Climate risk reporting is therefore not only about disclosure, it is about competitiveness and capital access.

Build capability in climate risk and ISSB, CSRD and VSME reporting

To address these challenges, we offer a Climate Risk Masterclass Series (available for Professional Members), led by expert practitioner Carlo Mancari, Principal Sustainability Consultant at Brightest.

The recorded 4-part series provides practical insight into:

- Climate Risk Fundamentals

- Physical Climate Risks

- Transition Climate Risk

- Reporting on Climate Risks

Using real-world examples and applied guidance, the series is designed to help professionals strengthen their understanding of climate risk assessment and reporting in practice.

Develop practical skills in ISSB reporting

To support professionals navigating this evolving landscape, the Sustainability Reporting Institute offers training designed to build practical capability in applying IFRS S1 and IFRS S2, alongside CSRD and GHG Protocol requirements.

Explore all free courses included with free membership, designed to build practical skills across climate risk, ESG reporting, and sustainability reporting standards here.

Included offerings:

- Free Introduction to the ISSB Standards

- Free CSRD Fundamentals course

- Free Introduction to the GHG Protocol course

FAQs on climate risk disclosure

- What is climate risk?

It is the potential for financial loss or business disruption arising from the effects of climate change whether from extreme weather events and shifting environmental conditions, or from the economic and regulatory changes involved in transitioning to a low-carbon economy. - What is the difference between physical and transition risk?

Physical risk comes from climate impacts like floods and heatwaves; transition risk comes from the shift to a low-carbon economy. - Is climate risk reporting mandatory under the CSRD?

Yes, the CSRD requires companies to disclose material climate risks under ESRS E1. - What is IFRS S2?

IFRS S2 is a global standard requiring companies to disclose climate-related financial risks and opportunities. - How do companies assess climate risk?

They use scenario analysis, climate models, and financial impact assessments across operations and supply chains.